US Inflation Is Cooling in 2026! What It Means for the Fed and the Dollar

The US inflation narrative in 2026 is no longer centred on whether price pressures are easing. The data increasingly confirms that they are.

The key question is whether it’s falling faster than official data shows, and whether the Federal Reserve’s current policy stance remains appropriate in a gradually cooling economy.

With headline inflation declining, the Fed on pause, and fresh debate emerging around labour market strength, markets may be approaching an important inflection point.

Inflation Is Slowing, But Housing Is Key

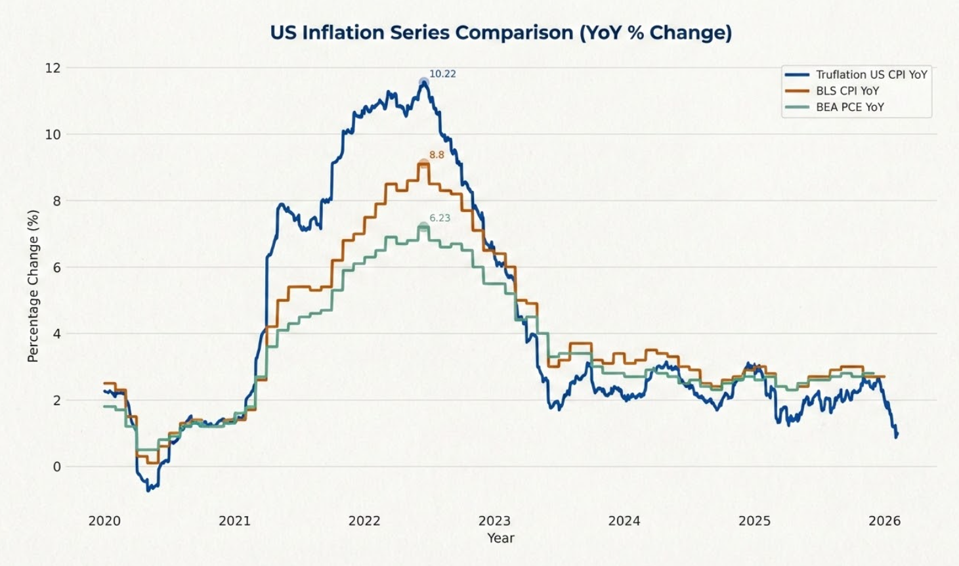

The latest Consumer Price Index (CPI) report showed headline inflation at 2.4%, marking the lowest level since mid-2025. Core inflation, which excludes food and energy, came in slightly higher at 2.5%, continuing its steady deceleration.

While these numbers suggest the Fed’s rate hikes are working, the shelter component, which makes up about a third of CPI, is lagging. The Bureau of Labour Statistics calculates shelter primarily through rent surveys and Owner’s Equivalent Rent (OER), which reflect lease agreements signed months earlier.

Real-time data shows rents have already slowed in many areas. As this is reflected in future CPI reports, inflation could fall even faster than expected.

High-frequency inflation trackers indicate that price pressures may already be running closer to 1% on a year-over-year basis, well below official CPI readings. Official CPI smooths price changes and uses lagging components, while real-time measures track current transactions and discounts.

If official inflation begins converging toward these real-time indicators, markets may need to reassess the trajectory of monetary policy, particularly at the short end of the yield curve.

The Fed On Hold But Not Fully Unified

The Federal Reserve started 2026 by maintaining the federal funds rate in the 3.5%–3.75% range, following three rate cuts in 2025.

Chair Jerome Powell stated that policy is not “significantly restrictive,” reinforcing a data-dependent approach. However, the January meeting revealed internal differences within the committee.

But some members, like Christopher Waller, are open to a March cut. More precisely, Fed Governor Christopher Waller suggested that recent labour market data may overstate underlying strength and indicated that support for a rate cut at the March meeting would depend heavily on upcoming employment figures.

Currently, markets see low odds for a March move, but everything depends on incoming data.

Is the Labour Market Losing Momentum?

Employment has been a key reason for the Fed’s caution. Yet recent developments point to moderation rather than acceleration.

Job growth has slowed compared with prior years, and gains have been concentrated in a limited number of sectors. Broader hiring activity remains subdued, even if widespread layoffs have not materialised.

Importantly, softness has emerged through reduced hiring rather than sharp increases in unemployment. This dynamic suggests gradual cooling, a development that may translate into slower wage growth and, by extension, lower services inflation over time.

If inflation continues easing while labour conditions soften further, the Fed’s current policy rate could begin to appear restrictive relative to economic momentum.

Base Effects Will Push Inflation Lower

Early 2025 had stronger monthly inflation. As those numbers drop out of the annual calculation and are replaced with softer 2026 readings, headline inflation will naturally decline, even if prices stay mostly stable.

Risks to the Disinflation Trend

While the disinflation scenario appears intact, risks remain.

Potential tariff adjustments, energy price volatility, sector-specific labour shortages, and structural shifts in electricity demand linked to AI development could create localised price pressures.

However, recent central bank communication suggests policymakers are inclined to look through temporary supply-side shocks unless they generate persistent, broad-based inflation.

As such, the primary focus remains on underlying inflation trends and labour market resilience.

US Dollar Outlook: Policy Expectations Now Lead

For the US dollar, the interplay between inflation, labour market conditions, and Federal Reserve policy is becoming the dominant driver.

- If inflation keeps falling and jobs weaken or are revised lower, markets may begin pricing earlier or more aggressive rate cuts. That scenario would likely pressure short-term Treasury yields and narrow interest rate differentials, and the USD could weaken.

- If inflation stays above 2.5% and jobs stay strong, the Fed may stay on hold, supporting yields and the dollar.

In short, the USD outlook in 2026 is increasingly tied to policy timing rather than inflation fear. Each CPI and employment release now carries greater significance, as even modest surprises could trigger meaningful repricing across currency markets.

What Traders Should Watch

The key catalysts ahead:

- February Non-Farm Payrolls

- Upcoming CPI releases (especially the shelter component)

- Any major revisions to 2025 employment data

- FOMC communication shifts

The dollar is no longer driven by inflation fear, it is driven by policy timing expectations.

If disinflation accelerates faster than the Fed signals, rate repricing could become the dominant FX driver in Q2 2026.

Conclusion

The macro narrative in 2026 is evolving.

Inflation is easing, but the pace of decline, particularly in shelter, may accelerate in the months ahead. At the same time, the labour market shows signs of gradual cooling. The Federal Reserve remains cautious, emphasising data dependence and balance. However, as inflation drifts closer to target and economic momentum moderates, the policy debate may shift from whether to cut rates to when.

For markets, the convergence between real-time inflation trends and official data may prove decisive. If that gap narrows quickly, expectations for monetary easing could adjust accordingly, with significant implications for yields, risk assets, and the US dollar.

Terms and Conditions apply

Click here to access our Economic Calendar.

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Andria Pichidi

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in Actuarial Science from the University of Leicester.

Following her various academic endeavours, Andria set eyes on the fascinating Forex industry where she has obtained valuable experiences after being active in the field for the past few years. In 2016, she joined HFM as a Market Analyst with a mission to actively support the company’s clients in becoming better traders, by delivering daily market reviews.